Chevron Stock Moved Past $200: What Should You Do With It Next? Just last year, we were talking with clients about Chevron in the $150–$160 range. It felt like Chevron had a good run. It felt constructive. But it didn’t feel like a major moment. Today, Chevron Corporation (CVX) is trading around $205—well clear of its ~ $160 200-day moving average. No one realistically thought we’d be above $200 / share in early 2026. Now the real question is: how do you turn this into something real—after taxes and in terms of what you actually keep? Past performance is not indicative of future results. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely for conducting investment research. The investment examples set forth in this presentation should not be considered a recommendation to buy or sell any specific securities. There can be no assurance that such investments will remain in the strategy or have ever been held in a WJA strategy. Why is Chevron Stock Going Up We all know, this is an oil story. Tensions with Iran and disruption risk around the Strait of Hormuz have pushed crude prices sharply higher. With uncertainty in oil supply, energy markets reprice quickly. Chevron’s stock price reflects that. This run isn’t due to any underlying business changes. It’s exposure to oil. Chevron’s Stock Outlook in 2026 Compared to Recent Years Chevron’s stock hasn’t been trending higher. Since mid-2023, the stock has been flat to down. A few reasons: Arbitration uncertainty with ExxonMobil Corporation over the Hess acquisition Rangebound-to-weaker oil prices for much of that period Questions around capital allocation and growth visibility How Oil Prices & the Iran Conflict are Impacting Chevron Stock So this recent move isn’t just continuation—it’s a reversal driven by an unexpended blockade of around 20% of the world's oil and gas. Consider this: if the key driver of the stock price is external, the outcome can change quickly. Oil prices moved almost overnight. They can also fall just as fast. If war in the middle east dies down and oil cools, Chevron likely follows. If tensions persist, it could move higher. You’re not just holding Chevron stock. You’re implicitly making a geopolitical bet on the length and magnitude on the war in Iran. Behavioral Investing: When Should I Sell My Chevron Stock? When people own stock that has made a significant run short-term, I often see people adjust price targets. Targets are easy to set when they’re abstract. Harder to execute in real-time. "I'll trim at $180." Then it hits $180... "Let's see if it runs." Now it’s $200. And the target moves again. This pattern repeats more often than people realize. Chevron Employees: CVX Stock Concentration Risk For many Chevron employees, they receive a significant portion of their annual compensation in Chevron stock. Through LTIPs, many hold: Stock grants Stock options (with built-in leverage and a clock) Option exercises often trigger ordinary income on the spread Selling vested shares typically results in capital gains (often long-term if held long enough) And this is where timing and taxes intersect. That means decisions here aren’t just about price: they’re about after-tax outcomes. A strong move like this can be an opportunity, but only if you’re thinking about what you actually keep. Diversifying Chevron Stock Exposure With Our Clients The conversation we’re having with clients is consistent: This may be a moment to take advantage of strength. That can look like: Exercising options while they’re meaningfully in the money (with a tax plan in place) Selling a portion of vested shares (and tax loss harvesting in the rest of the portfolio to offset the capital gains) Not all at once. Not reactively. Systematically and intentionally, using disciplined follow-through. For many people meeting with us, I’m asking, “If you had cash, would you be buying CVX stock today or something else?” The Takeaway If you wouldn’t be buying CVX stock with an extra $200, why are you continuing to hold it? Chevron being over $200 feels important. But what matters more is this: After a long stretch of sideways performance, you’ve been given a window. Between price, concentration, and taxes, this is one of those moments where a few simple decisions can change outcomes. If this is a position you’ve been meaning to revisit, it’s worth doing it now with both the market and the tax side in view. We’re happy to help you think it through.

Just last year, we were talking with clients about Chevron in the $150–$160 range. It felt like Chevron had a good run. It felt constructive. But it...

READ MORE

Nick Johnson, CFA®, CFP®

PRESIDENT & CHIEF INVESTMENT OFFICER

Shell Stock Crossed $90: Should You Hold or Sell in 2026? A few weeks ago, we were talking with clients about Shell in the $70s. And then, it actually happened: Shell crossed $90. It felt strong. It felt like progress. But it didn’t feel like a defining moment. Now, as I write this, Shell plc (SHEL) is trading around $91.88—well above its 200-day moving average of roughly $74. And now we’re having a different conversation with clients: what should you do with your Shell stock after a major market run-up like this, and is now the time to start selling Shell stock? Past performance is not indicative of future results. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely for conducting investment research. The investment examples set forth in this presentation should not be considered a recommendation to buy or sell any specific securities. There can be no assurance that such investments will remain in the strategy or have ever been held in a WJA strategy. Why is Shell Stock Going Up To think clearly about what comes next, it helps to separate this into two related drivers. A strategic re-rating that was already underway A geopolitical oil shock that accelerated the move Most commentary and headlines only focus on the second point, but the first is where the story really starts. Shell’s Strategic Shifts & Plans for Long-Term Growth Before the recent spike in oil, Shell had already been trending higher, and that wasn’t by accident. Under CEO Wael Sawan, Shell has become much more explicit about its priorities: Lower, more disciplined capital spending Higher shareholder distributions Continued cost reductions A clearer focus on LNG, oil, and gas Ongoing portfolio simplification At its latest Capital Markets Day, Shell outlined plans to keep annual investment in a tighter range, increase the percentage of cash flow returned to shareholders, grow LNG volumes, and reduce structural costs. For years, investors questioned how European energy companies would balance energy transition goals with profitability. Shell responded with a clear and focused strategy, and markets have responded. LNG & Oil Focus Driving Shell Stock Outlook Shell has not abandoned the energy transition, but it has become more selective about where it invests. Management has emphasized delivering “more value with less emissions,” prioritizing areas where the company believes it has a competitive advantage. In practice, that has meant leaning more heavily into: LNG and global gas demand High-return upstream projects Businesses with stronger, more predictable cash flow How Sale of Jiffy Lube is Impacting Shell Stock Another piece of the story is simplification. Shell has continued to sell non-core assets and streamline the business. Most recently, it announced the sale of Jiffy Lube for approximately $1.3 billion. Moves like this don’t usually drive a stock in the short term. But over time, they can support a higher valuation by: Simplifying the business Improving capital allocation Redirecting resources toward higher-return opportunities How Oil Prices & Iran Conflict Impact Shell Stock Outlook The recent move in Shell stock from the upper $70s into the $90s is much more directly tied to oil. The escalation in the Iran conflict and disruption in the Strait of Hormuz has pushed oil prices sharply higher. When oil moves like that, Shell’s stock price tends to move with it. That relationship is well understood and it’s the clearest explanation for the most recent leg higher. The recent run in Shell stock is driven by two different forces at once: A stronger, more disciplined business A commodity-driven spike layered on top This matters because strategic improvements may persist as Shell doubles down on their competitive advantage, but the spikes in energy are less predictable over time. A de-escalation, reopening of shipping routes, or normalization in crude prices could bring energy prices back down. If that happens, Shell could still be a stronger company than it was two years ago. But what does this mean for investors holding Shell stock? Behavioral Investing: When Should I Sell My Shell Stock? This is where investing gets interesting. Not long ago, for many investors, the number wasn’t $90. It was $80. “If Shell gets to $80, that would be an amazing opportunity to sell.” That felt like the win. The nice run. The moment to reduce exposure. And then it happened. Shell moved through $80. And instead of selling, the conversation changed: "Let's see if it gets to $90." "Oil is strong, this might have more room." "This isn't the right time anymore." The target moved. This is a very human pattern. The level that once felt like the finish line quickly becomes the new baseline and a new target appears just beyond it. The Risk of Holding Shell Stock Too Long The risk is not that the stock goes higher. It might. The risk is that the plan quietly fades into the background and disappears. Some investors were waiting for $70. Then $80. Now $90. Next, it may be $100. And at each step, the same logic applies: “Just a little bit more.” If you had a plan built on strategy and told yourself: “When Shell gets to $80, I’m going to diversify a portion of my holdings” Then this is the moment to revisit that plan honestly. How we like to look at it from an objective approach: “If you had cash, would you be buying Shell stock today or something else?” That answer tends to clarify things quickly. If the answer is: "Something else" why don't you sell and diversify "My situation has changed" that's worth evaluating "I just feel like holding on a bit longer" that's where behavior tends to take over Diversifying Shell Stock Exposure We’re having a lot of conversations right now with Shell executives and professionals who have benefited from this recent run-up. In many cases, our recommendation is consistent: Use the strength to diversify. Not because Shell is a bad company. Not because the stock can’t go higher. But because moves like this, especially when influenced by geopolitics—don’t tend to last forever. When the war in the middle east ends, it could likely do so quickly, with the opportunity to sell at today’s prices in the rear-view mirror. How Shell Stock Compensation Impacts Your Decision For many Shell employees, this timing is particularly relevant. A lot of clients have just received new shares in Q1 through: Performance Share Plans (PSP) GESPP purchases At the same time, many still have granted but unvested shares that will continue to vest over the next several years. This means even if you sold everything that’s fully vested today, you would still remain meaningfully exposed to Shell through future vesting and performance-based compensation. And that’s before you factor in your exposure from your base salary, bonus compensation, and pension all being tied up in the same company! You’re not walking away from all the upside. You’re simply reducing concentration risk today. Want to go deeper? We’ve written more about how Shell compensation works and how to think about diversification and taxes around Performance Shares and the GESPP: https://insights.wjohnsonassociates.com/blog/shell-stock-compensation-shell-shares

A few weeks ago, we were talking with clients about Shell in the $70s. And then, it actually happened: Shell crossed $90. It felt strong. It felt...

READ MORE

Nick Johnson, CFA®, CFP®

PRESIDENT & CHIEF INVESTMENT OFFICER

4 Ways to Invest Your Chevron Incentive Plan (CIP) Bonus time can be exhilarating – a large lump sum of cash that Chevron employees can use for many expenses – paying off debt, taking a vacation, or hiding under the mattress for a rainy day. But for Chevron super-savers, there are many additional strategies to help you optimize your bonus payout. What is the Chevron Incentive Plan (CIP)? The Chevron Incentive Plan (CIP) is Chevron's short-term cash incentive program. Colloquially, many Chevron employees refer to the CIP as the annual Chevron bonus. Chevron CIP Formula & Calculation Factors Chevron bases an individual's CIP bonus on the employee's job grade, individual performance, and the company's annual performance. Chevron reviews many factors when determining company performance, including comparing the company to top performers in the Oil Industry Peer Group. In 2026, we expect to see a lower bonus payout than in recent years, as Chevron's earnings declined in 2025 compared to the previous year. With this impending bonus payout for Chevron employees, it is important to note how this additional income will impact your cash flow, retirement savings, and taxes. How is Your Chevron Bonus Taxed? When you receive your bonus, it's an excellent time to check in on your tax withholding. It's essential to know that you are withholding enough in taxes from your paychecks and bonuses, so you do not need to make an estimated tax payment for Q1. The last thing you want to deal with is an additional tax penalty on top of your tax bill come April 2027. Additionally, since CIP payouts are considered supplemental income, they are taxed differently than ordinary income. The IRS taxes supplemental income, like bonuses, up to $1 million at a flat withholding rate of 22%. If you are a high-income earner at Chevron, 22% may not be enough withholding to cover your tax bill without additional penalties. Therefore, it's essential to work with a tax professional who can check in on your ongoing tax withholding and help you calculate any extra payments you may owe after you receive your bonus. How the CIP Impacts the Chevron Pension (CRP) If retirement is near the horizon, consider how your next CIP payout may affect your pension calculation. The Chevron Retirement Plan (CRP) formula considers your years of service and Average Final Compensation (AFC). If either of those variables increases, the pension value increases. Chevron averages the 36 most highly compensated consecutive months in the last ten years when reviewing AFC for an upcoming retiree. A larger bonus payout for this year could increase the AFC over the previous 36 months for an impending retiree. For the CRP calculation, a crucial caveat is that Chevron employees who want their AFC to include the March 2026 CIP payout must be on the U.S. payroll for at least one day in April 2026. Chevron provides retirees with prorated bonuses for work completed in their year of retirement, so long as the employee works for at least one day in the next quarter. So, for example, if someone retired on July 1st, 2026, they'd receive a 50% prorated bonus, and if they retired on October 1st, 2026, they'd receive a 75% prorated bonus. Given that timeline, it would be prudent to review your AFC and determine whether it would be valuable to stay on the payroll until the first day of an upcoming quarter to maximize the AFC for your pension. How to Invest Your Chevron Incentive Plan Payouts When talking to Chevron supersavers, a common question arises, “should I invest my bonus or save it in a certain account?” The answer depends on an individual’s unique circumstances and goals. However, the following strategies are considerations we discuss widely as ways to consider leveraging the CIP payout in March. Invest Excess Cash To Avoid Tax Drag from Inflation Having a cash reserve for emergencies is critical to sound financial planning, but carrying too much cash can be detrimental to a plan. You need to earn 2.6% from investments to break even on the purchasing power of your cash if we look at the inflation numbers from December 2025. With the CIP payout in March 2026, it would be prudent to review your cash holdings and determine if you should reinvest any funds, with the goal to achieve growth that outpaces inflation. And with the market currently pulled back from all-time highs, investing cash in this pullback could be a strategic investment opportunity. Make Contributions to Your Chevron 401(k) Since the bonus payouts occur in March, you should plan to check your 401(k) contributions before and after the bonus payout. You may consider contributing more to pre-tax or supplemental with your CIP payout, especially if you know you will reach or exceed 2026's income limit of $360,000 before maxing out your ESIP. Front-loading contributions with the CIP will help make sure you max out your pre-tax, after-tax, Roth and company contributions before reaching this $360,000 income limitation. After the bonus payout, you will want to check your year-to-date ESIP contributions to determine if you need to adjust your future supplemental contribution percentages to max out pre-tax contributions of $24,500 if you are under and over 50. If you're over 50, you can do the $8,000 catch-up into a Roth, as well as your after-tax contributions. Your total after-tax contribution amount will vary annually depending on your salary and CIP payout. Your total after-tax contribution amount is the difference between the overall 401(k) contribution limit and the sum of your pre-tax and Roth contributions and your 8% company match (if contributing 2% to basic). Leverage Backdoor Roth Contributions You have several options for where you can invest excess cash. For example, if you've maxed out your 401(k), you may consider contributing to an after-tax account or making a backdoor Roth contribution. A backdoor Roth contribution allows you to roll your excess cash over into a Roth IRA to take advantage of long-term tax-free growth, even if you're above income limits that prevent you from directly contributing to a Roth. Backdoor Roth Contributions allow individuals to make a nondeductible IRA contribution of $7,500 if under 50 or $8,600 if over 50. Once you contribute to the IRA, you convert the IRA to a Roth IRA. Once funds are available in the Roth IRA, you can invest the cash in an allocation designed for growth, which can be a great solution to get cash working towards tax-free growth. There are currently no income limits on nondeductible IRA contributions; therefore, individuals who are over the income limit for direct Roth IRA contributions can still use this Backdoor Roth strategy. Reduce Taxable Income Through Charitable Giving A more significant bonus may result in a higher-than-average income year and a significantly higher tax bill. While working, you can pull a few levers to minimize your tax bill – max out pre-tax retirement savings accounts, deduct property taxes up to or at least $10,000 based on your income, deduct mortgage interest on up to $750k of debt for mortgages after 2017, and deduct charitable donations. Starting in 2026, provisions from the One Big Beautiful Bill Act include a 0.5% floor on charitable contribution deductibility, creating additional complexity in tax planning. If you are charitably inclined, making a significant charitable gift in a year of high income can be incredibly beneficial to lowering your tax bill. You could consider direct contributions to a charity or a Donor-Advised Fund (DAF) to bundle your charitable gifts into more significant lump sum donations. To optimize the tax efficiency of your contribution, consider donating appreciated stock instead of cash. You can gift appreciated stock directly to a charity or a DAF, which offers you an itemized deduction on your tax return and avoids the capital gains taxes on the stock. With your cash CIP payout, you can replace the stock value with cash and either reinvest in the same stock or diversify elsewhere. OptimizeYour Investment Strategy by Working with a Financial Advisor CIP payouts every spring are exciting, but it's important to invest them in the things that matter most to you and your family. At Willis Johnson and Associates, we can help optimize your annual performance bonus for the journey ahead through tax planning, savings prioritization, and benefits eligibility assessment. Partnering with an advisor who understands your financial needs for today can be instrumental in helping you establish financial systems to support your future goals. Get started today by discussing your financial goals and Chevron benefits with the advisors at WJA, who can offer tailored guidance to help you reach financial independence.

Bonus time can be exhilarating – a large lump sum of cash that Chevron employees can use for many expenses – paying off debt, taking a vacation, or...

READ MORE

Alexis Long, MBA, CFP®

MANAGING DIRECTOR, WEALTH MANAGEMENT

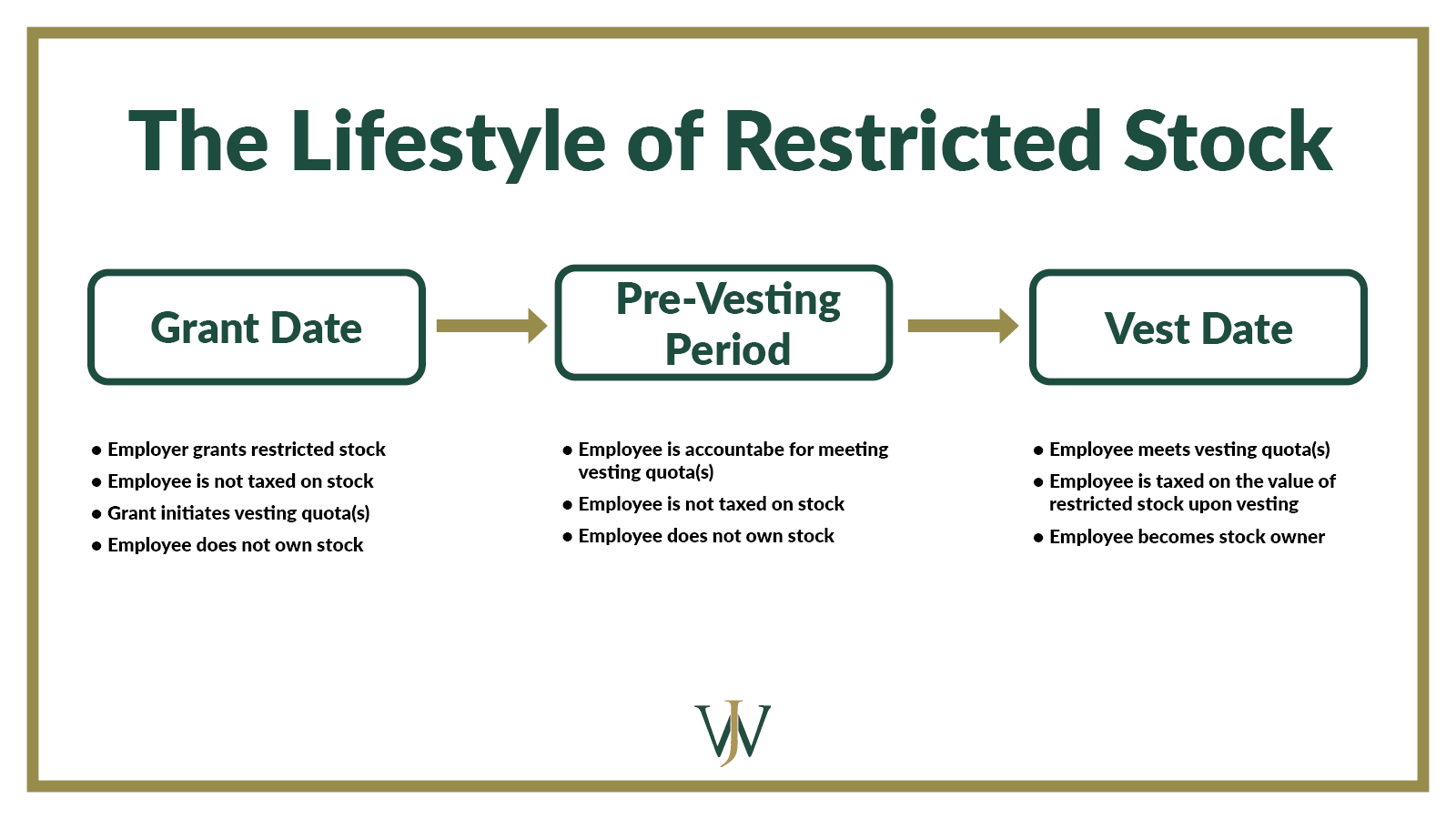

How to Avoid Double Taxation on Restricted Stock Units (RSUs) If you’ve worked for Dow, Shell, Chevron, BP, or other major oil companies for several years you may receive Restricted Stock Units (RSUs) or other company share awards as part of your executive compensation package. The value of the RSUs you receive is included in your W-2 as compensation in the year you receive the shares. Far too often, when we review a professional’s tax returns, we discover that the executive (or the CPA preparing their return) has used the incorrect basis when selling RSUs. Unfortunately, when they sell the RSUs a few years later, they end up paying taxes twice! And…who really wants to pay more to the IRS than what is required? In this article, we’ll cover how this costly mistake arises and how to fix it to get a refund of money you overpaid to the IRS, so let’s dive in. What are Restricted Stock Units (RSUs)? Restricted stock units are a form of employee compensation via company shares that an employer gives to employees on a predetermined vesting and distribution schedule. Many oil and gas companies have different names for these plans, some given by the companies themselves and others by the employees receiving them. For example: At Shell, many employees refer to RSUs by a few different names including Shell Performance Awards, Shell Stock Awards, and "Share Grants." At BP, these are known as Restricted Share Units as part of BP's overarching Share Value Plan. Within the Share Value Plans at BP, employees may also have Reinvent Options or Performance Shares, which are beyond the scope of this article. At Chevron and at Dow, RSUs are called by their name: Restricted Stock Units, or RSUs for short. When these RSUs are granted, the value of the shares is considered compensation income for the year you received them. Compensation income is considered “ordinary” income and is taxed at regular tax rates. RSUs are not considered a capital gain or passive income and, therefore, are not taxed at preferential capital gains taxes. RSUs & Ordinary Income Taxation Let’s use an example to illustrate taxation on restricted stock units. Suppose you are a Shell professional who’s been granted the following RSUs throughout the years. Remember, the values of the shares at the time of grant were included in your Form W-2 as compensation income the year you received them. Date of Grant Number of Shell RSUs granted Value per share at the time of grant Value included on your Form W-2 01/01/15 155 $57.59 $8,926.45 03/08/16 497 $70.96 $35,267.12 03/13/17 587 $72.18 $42,369.66 03/12/18 536 $65.98 $35,365.28 02/27/19 410 $72.90 $29,889.00 02/17/20 463 $66.40 $30,743.20 03/01/21 364 $46.44 $16,904.16 03/01/22 590 $52.35 $30,886.50 03/02/23 539 $63.09 $34,005.51 03/01/24 2,268 $62.32 $141,341.76 03/04/25 1,566 $45.21 $70,798.86 Total shares granted 7,975 $476,497.50 Through the years, your Forms W-2 have reported a total of $476,497.50 in taxable compensation from your RSUs. Let’s suppose you reported the income from your W-2 ($476,497.50) on your tax returns each year and have been fully taxed on each year’s stock grant. Because you’ve been taxed on this income, you should include that compensation income from the yearly grants into your cost basis of the shares. Discovering Double Taxation on RSUs Using Form 1099-B To continue the example, in May 2026, let’s suppose you retired from Shell. In December, you decided to sell all 7,975 shares to diversify your portfolio. The market was lower then, and it seemed like a good time to buy into other investments. The total proceeds for the sale of all 7,975 shares were $299,145.74, which are reflected in your 2025 Form 1099-B as shown below: Form 1099-B has been prepared per the IRS reporting requirements and is correct. And, because you didn’t pay anything for these shares when they were granted to you through the years, it makes sense to you that the cost basis shows $0 for all the shares. When preparing your tax return for 2025, you enter these sales with a cost basis of $0 and recognize a long-term capital gain of $299,145.74, which results in the following tax amount: 20% capital gains rate tax on gain from RSU sale $59,829 3.8% net investment income tax on gain from RSU sale $11,368 The total amount of tax that you will pay on the sale of the Shell Performance Shares is $71,197, which is quite a substantial amount of tax. All this seems pretty straightforward, right? It’s “just using the information on Form 1099-B for your tax return.” What could possibly go wrong? By following these steps, as straightforward as they seem, you've actually made a costly mistake — Double-Taxation. RSU Income is Not Reflected as a Cost Basis Let’s take a closer look at the small print on Form 1099-B. In the cost basis column, there is a little code “e” followed by very specific and important conditions. This small print acknowledges that the shares that were sold were acquired through the employer stock plan. “Cost basis associated with these shares may not have been adjusted for any compensation income that was associated with those shares in the year of acquisition.” This small print states that the Form 1099-B cost basis does not include the previously-taxed compensation income that was included in years of Forms W-2. This previously taxed income should be included in the cost basis. Most taxpayers (and sometimes even their CPAs) report exactly what is shown on their Form 1099-B when they prepare their yearly tax returns. However, a little-known regulation of the IRS is that brokers (like Fidelity, Edward Jones, UBS, Charles Schwab, etc.) are not allowed to include “ordinary” income on Forms 1099-B. This is why, in our example, Form 1099-B reflects only $0 as a cost basis. How to Prevent Double-Taxation on Your RSUs What is the solution? Many brokers, like Fidelity, provide important details in their Supplemental Information included in the last pages of the yearly Forms 1099-B. Taxpayers (and their CPAs) must look beyond Form 1099-B and into this Supplemental Information for information that will prevent double taxation. Use Supplemental Information from Brokerage Firms Fidelity has online resources to walk taxpayers through both Forms 1099-B and the accompanying Supplemental Information. You will need both Form 1099-B and the Supplemental Information section included with your Form 1099-B when you prepare your tax return. Continuing with our example, the following information is included in the Supplemental Information of your Form 1099-B for 2025: You can see the column “Ordinary Income Reported,” which reflects the amount of income that was included in your Form W-2 through the years. Note that the same amount is included in the column “Adjusted Cost or Other Basis”. Once you include the cost basis in the calculation of the gain, the result is actually a long-term capital loss (LTCL) of $177,351.79! Impact of Double Tax on RSUs This loss can offset current and future long-term capital gains, which, assuming a 20% capital gains rate plus the 3.8% net investment income tax, will save $42,210 in taxes. Additionally, you will save yourself from paying the $71,197 in tax by not including the cost basis in the calculation. Double-Taxation Cost of Using $0 Cost Basis $(71,197) Tax Savings from Using Supplemental Info Cost Basis, Resulting in LTCL Carryover $42,210 In this example, the total double-taxation costs are the following: 1) current year tax of $71,197, and 2) the foregone tax savings from the loss of $42,210. That’s a whopping $113,407 in tax costs! Uncovering Double Taxation on RSUs We’ve seen how quickly this mistake can add up in a given year, so you may ask, “Did I make this mistake?” Here’s how you can find out: First, dig through your closet or search the files on your computer for your past three years of tax returns. Next, log into your brokerage account for the complete Forms 1099-B for the three years, including the Supplemental Information section. Then, take these steps: In your tax return, locate Form 8949, Sales and Other Dispositions of Capital Assets. Search for the sale of the specific RSUs and identify the amount shown in column (e) for Cost Basis. In the Supplemental Information section of your Form 1099-B, find the adjusted cost basis for the corresponding sale of the RSUs. Determine if these numbers are the same. If so, your tax return was completed correctly. If the numbers do not agree, you likely have an error on your return, which may have caused you to pay more tax than necessary. How to Address Double Taxation on Previous Tax Returns If this error exists on a prior year’s tax return, you can amend the three most recently filed tax returns by filing a Form 1040-X, Amended U.S. Individual Income Tax Return. Filing an amended return will permit you to correct the basis and get a refund of any taxes you have overpaid. Three years is the statute of limitations on filing an amended return. If you amend a return to correct the error, it must be filed within three years of that return's original filing date. The following tables illustrate the periods you have to file an amended return, assuming you filed on or before the April 15 due date: 2025 tax return April 15, 2029 2026 tax return April 15, 2030 2027 tax return April 15, 2031 Working with a Tax Professional Can Help You Avoid Double Taxation If your cost basis is incorrect and a CPA or other tax professional prepared your return, reach out and request that they review the return and file an amended return on your behalf. If you prepared the return yourself, you will likely need professional assistance to file an amended return. For WJA clients, we offer a complimentary review of your tax return to identify whether the sales of RSUs or other performance shares have been reported correctly. Our in-house tax department routinely provides this service to provide our clients with high-quality, year-round tax planning and compliance. If you have any questions about whether you have been double-taxed on selling your RSUs or performance shares, act now. The stakes are high. You should not pay more to the IRS than is required. Schedule a conversation with an advisor today to discuss your tax situation and its role in your overarching financial plan.

If you’ve worked for Dow, Shell, Chevron, BP, or other major oil companies for several years you may receive Restricted Stock Units (RSUs) or other...

READ MORE

Leah Cessna, CPA

DIRECTOR OF TAX

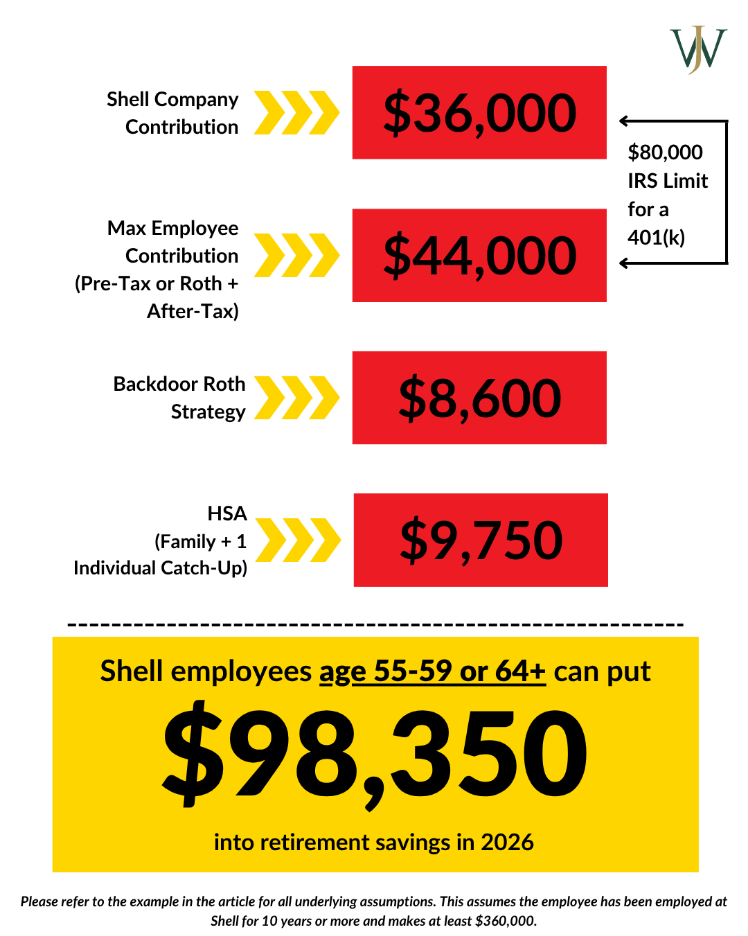

5 Ways to Get More From Your Shell Bonus This Year Bonus season is finally here! From dream vacations to visions of paying off expenses, your hard-earned bonus holds exciting potential. For Shell super-savers seeking to make the most of their bonus, the clock starts ticking the moment it hits your account. This spring, unlock the full power of your bonus with strategies devised to help you reach your financial goals, invest for future growth, or simply make your bonus work smarter for you. Shell Bonus Formula & Calculation Factors To determine an individual’s bonus, Shell looks at three factors: The employee's job grade with a target bonus, individual performance, and the company's annual performance. When evaluating company performance, Shell reviews financial targets and their performance in the industry to determine the company’s bonus factor. In the years where Shell performs well, the bonus payouts have been higher. For some employees, Shell awards spot bonuses for exceptional individual performance in managing or completing company strategies. In 2026, we expect to see a relatively positive bonus payout compared to recent years. Shell’s adjusted earnings for 2025 were $18.5 Billion. With this anticipated shift in payouts for Shell employees, there are strategies and opportunities to consider. How is the Shell Bonus Taxed? Bonus season is the perfect opportunity to do a tax tune-up and review your withholdings. Why? Because you want to avoid two possible surprises come April: a hefty tax bill, or a potential penalty. Remember, bonuses are treated differently than regular income. They're considered "supplemental income," and the IRS takes a flat 22% out of them for supplemental income up to $1 million. As a high-income professional at Shell, withholding 22% might not be enough to cover your full tax bill. That's where working with a professional tax team comes in—They can assess your current withholdings and calculate any additional payments you may need after your bonus hits to avoid penalties. One way to think of it is as an investment in your peace of mind, avoiding last-minute scrambles and unnecessary fees. How the Shell Bonus Impacts Pension Payouts At Shell, you have two pensions that you may be eligible for depending on when you began employment: the 80 Point Pension and the APF Pension. For either pension, your average final compensation (AFC) plays a crucial role in the calculation of your benefit. The higher your AFC, the higher your pension benefit at retirement. Specifically, Shell uses the highest three years of average final compensation within the last ten years to determine your pension payout. One thing many Shell professionals notice when evaluating their AFC over the last ten years is the impact COVID had on their annual compensation in 2020 and 2021. If you recall, due to the global shutdowns and the energy sector’s performance in those years, many Shell professionals received minimal bonuses or no bonus at all. However, if we fast forward to 2023 and 2024, we saw a huge rebound in energy. As a result, many Shell professionals received promotions, salary increases, or higher-than-average bonuses. However, in 2025, Shell's earnings were down by about 11%, so strategically evaluating your AFC in light of these shifts can significantly impact your pension calculation. If your retirement date from Shell is flexible, waiting until you receive your 2025 bonus payment in 2026 to retire could be crucial so your pension calculation includes this higher AFC number. Investment Strategies for Your Shell Incentive Plan Payout Many Shell professionals come to us with the same question: "With my annual performance bonus on the horizon, should I invest it or keep it in a savings account?" As with every financial decision, the answer truly depends on your circumstances and future goals. However, there are several popular strategies that Shell professionals often consider after receiving their payout each March. Let's delve into some of these options: Contribute to the Provident Fund Because the bonus payouts are in March, you should plan to check your Shell Provident Fund contributions before and after the bonus payout. In 2026, you can contribute up to $24,500 if you’re under 50 to either pre-tax or Roth sources in the 401(k). If you're over age 50, you're eligible to make catch-up contributions to your 401(k). If you’re age 50-59 or over age 64, you can contribute up to $32,500 for this year. If you're age 60-63, you can contribute up to $36,000 in 2026. However, if your income exceeded $150,000 in 2025, any catch-up contributions must be designated as Roth contributions. Beyond the pre-tax and Roth sources in the 401(K), it's essential to check your year-to-date 401(k) contribution percentages to maximize the after-tax source. The maximum amount you can contribute to Shell’s after-tax source in 2026 is $11,500. Making 401(k) Contributions Directly from Your Bonus Let’s say you want to use your bonus to make 401(k) contributions this year in hopes of maxing out all sources in the Provident Fund. If so, you must set up those elections in Fidelity before the bonus gets distributed. Even if you’re making contributions from your paycheck, the default election for bonus contributions to the 401(k) is 0%. If you know you will reach or exceed 2026's income limit of $360,000 this year, you can consider front-loading your contributions from your paycheck and bonus to ensure you max out the 401(k) before exceeding the threshold. For high-income Shell employees, this can make a HUGE difference in how much they can save each year. Once an employee crosses the threshold of the IRS’s 415 income limits, neither Shell nor the employee can contribute to the 401(k). So, if you receive a significant bonus but don’t make contributions to the 401(k) from it, you may be leaving a lot of money on the table for retirement. Learn how to max out your Shell 401(k) this year here >> Get Invested: Don’t Sit on the Cash Inflation numbers are at 2.6% as of December 2025, which means that due to ongoing inflation, any cash is effectively losing purchasing power by 2.6%. To have a sound financial plan, holding some cash-on-hand is necessary for emergencies, but carrying too much cash can be detrimental to a plan. To break even on your cash’s purchasing power, you need to earn 2.6% on investments. With the approaching bonus payout in March 2026, it would be well-advised to review your cash holdings and determine if you should reinvest any funds, with the goal to achieve growth that outpaces inflation. Leverage Backdoor Roth Contributions There are several options available for where you can invest excess cash. For example, if you've maxed out your 401(k), you can contribute to an after-tax account or make a backdoor Roth contribution. If you are a high-income earner, you probably already know that you can’t contribute directly to a Roth IRA. The backdoor Roth contribution strategy is a way to get around the income limitation and still save money in a Roth IRA. With a backdoor Roth contribution, you can roll your excess cash over into a Roth IRA, where that money can grow tax-free in the long term, even if you’ve surpassed the income limits that prevent you from directly contributing to a Roth. With backdoor Roth contributions, you can make a nondeductible IRA contribution of $7,500 if under age 50 or $8,600 if over 50. After you have contributed to the IRA, you convert the IRA to a Roth IRA and enjoy tax-free growth for life. Mega Backdoor Roth Strategy If you are contributing after-tax dollars to the Shell Provident Fund, you can also roll out the after-tax funds annually to a Roth IRA to take advantage of a strategy known as the mega backdoor Roth strategy. When you make after-tax contributions in your Shell Provident Fund 401(K), you have two options for what you can do with those funds: leave them in the 401(K) or roll them out via a Roth conversion to a Roth IRA. If you leave the funds in the 401(K), at withdrawal, your contributions will be tax-free, and any growth you accumulate will be taxed at ordinary income rates. That’s not too tax-efficient. If instead, you annually roll the after-tax funds over to a Roth IRA, the growth and contributions grow tax-free for life! Learn More About the Mega Backdoor Roth Strategy Here >> Reduce Taxable Income Through Charitable Giving While a noteworthy bonus may bring delight, it can also result in a higher-than-average income year and a significantly higher tax bill. You can strategically pull a few levers while you're working to minimize your tax bill – max out pre-tax retirement savings accounts, deduct property taxes up to $10,000, deduct mortgage interest on up to $1m of debt, and deduct charitable donations. Starting in 2026, provisions from the One Big Beautiful Bill Act include a 0.5% floor on charitable contribution deductibility, creating additional complexity in tax planning. Like many of our clients, you may be charitably inclined, and making a significant charitable gift in a high-income year can be incredibly beneficial to lowering your tax bill. Some options include - direct contributions to a charity or a Donor-Advised Fund (DAF) to bundle your charitable gifts into more significant lump-sum donations. Advisor tip - To maximize the tax efficiency of your contribution, you can donate appreciated stock instead of cash. In addition, gifting appreciated stock directly to a charity, or a DAF offers you an itemized deduction on your tax return and avoids the capital gains taxes on the stock. With your bonus payout, you can replace the stock value with cash and either reinvest in the same stock or diversify elsewhere. Optimize Your Investment Strategy by Working with a Financial Advisor The annual bonus payout is a well-deserved reward for your hard work at Shell. But amidst the excitement comes an important question: how can you leverage this benefit to propel yourself and your family toward your financial goals? At Willis Johnson and Associates, we understand the unique needs of Shell employees. We partner with you to help you make the most of your bonus each year, keeping your goals, tax implications, savings priorities, and other benefits top-of-mind. As a planning-led firm, our advisors are equipped to: Leverage your benefits: Maximize the value of your Shell benefits and compensation package so you don't leave any money on the table. Craft a personalized strategy: Once we know what’s available to you, we delve into your financial aspirations and current tax situation so we can tailor solutions that fit your individual needs. Navigate the tax landscape: Ensure you keep more of what's yours by leveraging tax strategies to lower your tax burden over time. Prioritize savings: Identify the most impactful savings vehicles to achieve your short- and long-term goals. Investing in your future starts today. Our experienced advisors can help you establish a robust financial plan for any stage of life. Our goal is to make the complex simple so you can achieve financial freedom, whether it's planning for retirement, caring for loved ones, or donating to the charities you care about most. Get started by scheduling a complimentary consultation with the advisors at WJA. We’ll discuss your financial goals and Shell benefits, and together, we'll craft a personalized plan to help you achieve financial independence and fuel your future success.

Bonus season is finally here! From dream vacations to visions of paying off expenses, your hard-earned bonus holds exciting potential. For Shell...

READ MORE

Brandon Young, CFP®

WEALTH MANAGER

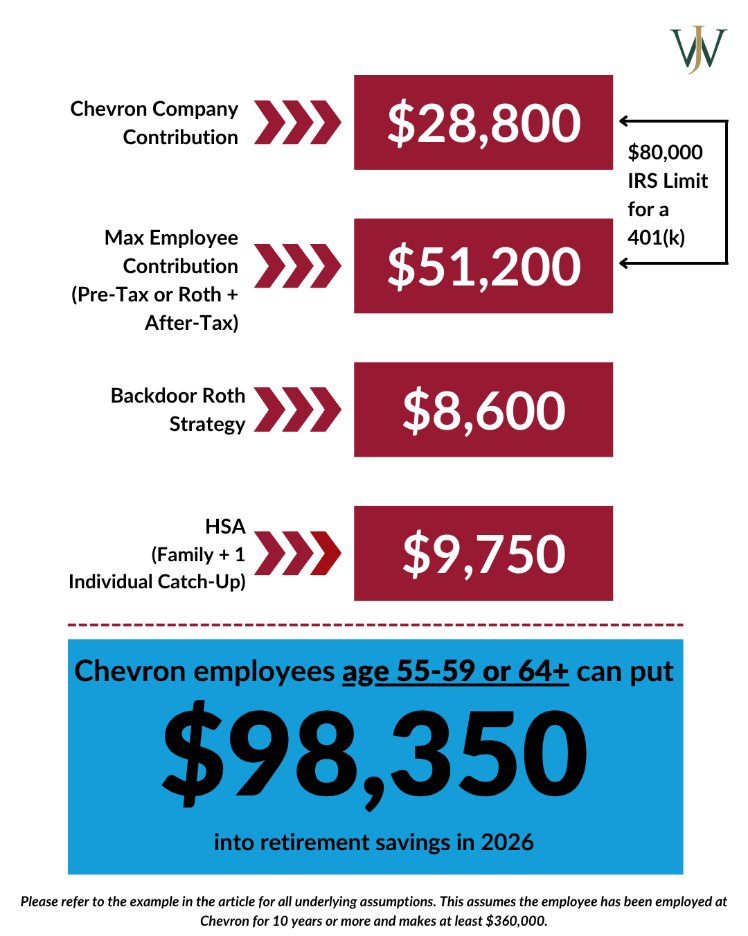

5 Opportunities for Your BP Annual Cash Bonus Bonus time can be thrilling – having a large amount of cash on hand to fund expenses such as paying off debt, taking a vacation, or hiding it under the mattress for a rainy day. But for BP super-savers who want to maximize their bonus payout, there are many additional strategies to leverage this spring. BP Annual Cash Bonus (ACB) Formula & Calculation Factors BP bases an individual's ACB bonus on the employee's job grade, with a target bonus, individual performance, and the company's annual performance. BP reviews many factors when determining company performance, based on performance and financial targets, and BP’s performance within the industry. In those years in which BP's performance has been high, the bonus payouts have been higher. BP also awards spot bonuses for exceptional individual performance in managing or completing Company strategies. As BP continues to make progress on its longer term goals, we anticipate bonus performance calculations to be higher this year — in the 1.5 factor range. Personal and group target bonuses may be higher. When we engage with BP employees, we explore strategies and opportunities for planning, including their bonus outcomes. How is Your BP Bonus Taxed? Receiving your bonus is an excellent time to revisit and look over your tax withholdings. To avoid making an estimated tax payment for Q1, it is essential to ensure that you are withholding enough in taxes from your paychecks and bonus. Dealing with an additional tax penalty on top of your tax bill in April 2027 is not something you want to be dealing with. Bonus payouts are taxed differently than ordinary income because they are considered supplemental income. The IRS taxes supplemental income, like bonuses, up to $1 million at a flat withholding rate of 22%. As a high-income earner at BP, 22% withholding may not cover your tax bill without additional penalties. Therefore, working with a tax professional who can check in on your ongoing tax withholding and help you calculate any extra payments you may owe after you receive your bonus is crucial. How the BP Bonus Impacts the BP RAP Pension If you are gauging your pension as a factor in your retirement, you should consider how your next ACB payout may affect your pension calculation. The BP RAP formula considers your years of service, age, and your annual compensation. If you are over 50 with 20 years of service at BP, you are credited with up to 11% of your eligible pay, including base pay and annual cash bonus (not spot bonus or other incentive pay). So, a major uptick in cash compensation can create a significant increase in the cash balance of your RAP Pension. How to Invest Your BP Incentive Plan Payouts A common question we often hear when talking to BP supersavers is, “Should I invest my bonus or save it in a certain account?” This answer is contingent on an individual’s unique circumstances and goals. The following strategies are discussed widely as ways to consider leveraging the ACB payout each spring. Invest Excess Cash To Avoid Tax Drag From Inflation To have a sound financial plan, holding some cash-on-hand is necessary for emergencies, but carrying too much cash can be detrimental to a plan. You need to earn 2.6% from investments to break even on the purchasing power of your cash, looking at inflation numbers from December 2025. With the approaching ACB payout in March 2026, it would be well-advised to review your cash holdings and determine if you should reinvest any funds, with the goal to achieve growth that outpaces inflation. Make Contributions to Your BP 401(k) Because the bonus payouts are in March, you should plan to check your 401(k) contributions before and after the bonus payout. If you know you will reach or exceed 2026's income limit of $360,000, you can consider contributing more to pre-tax with your ACB payout before you max out your ESP. Front-loading contributions with the ACB will ensure you max out your pre-tax, after-tax, and company contributions before reaching this $360,000 income limitation. After the bonus payout, it's important to check your year-to-date ESP contributions percentages to not only max out your after-tax contributions but max out pre-tax contributions of $24,500 if you are under 50 or $32,500 if you're over 50. Factors, including your salary and the amount of your ACB payout, will vary your total after-tax contribution amount annually. Your total after-tax contribution amount is calculated by taking the difference between the overall 401(k) contribution limit, the sum of your pre-tax contributions, and your 7% company match. For example, Sheri is a BP professional, age 54, whose base salary is $280,000 and whose target bonus is 40%. Figuring that she will fill out her pre-tax bucket and after-tax bucket over the full year, she decides to elect 18% of her base salary to defer into the 401(k), so she will contribute both the full pre-tax and the after-tax by December. However, Sheri’s bonus, even without any performance factor, will push her total compensation to almost $400,000. By October, when Sheri hits the compensation limit of $360,000, she can no longer contribute to the 401(k). …But Don’t Over-Contribute to your 401(k) After the bonus payout, you will want to check your year-to-date ESP contributions to determine if you are about to over-contribute. Due to BP’s 401(k) spillover provisions, your continued contribution, either pre-tax or after-tax, can push BP’s contribution to the plan into the Excess Benefit Plan (EBP). The EBP is a non-qualified plan with more stringent restrictions, which poses a challenge for financial planning. For example, Trevor, age 51, has a compensation structure similar to Sheri (in the example above) - a $280,000 base with a 40% bonus target. He is well aware that he will top out on his compensation limit, so he sets his deferral to the 401(k) at $33% to max out his pre-tax and after-tax by well ahead of hitting the compensation $360,000 limit. He succeeds. By April, he has contributed fully to the after-tax and the pre-tax. However, Trevor does not adjust his contribution because he does not know about the spillover provisions in the 401(k) plan. As such, he continues to make after-tax contributions and does not notice because he is busy with his job. Dollar for dollar, these contributions begin to “push out” the BP contribution to the 401(k) and into the Excess Benefit plan. While Trevor can still save quite a bit for retirement this way, pushing funds into the EBP isn’t optimal for long-term financial planning. The EBP has unique distribution rules he’ll need to plan around in the future, so keeping an eye on contributions before they spill over would be more optimal. Leverage Backdoor Roth Contributions There are several options available for where you can invest excess cash. For example, if you've maxed out your 401(k), you can contribute to an after-tax account or make a backdoor Roth contribution. With a backdoor Roth contribution, you can roll your excess cash over into a Roth IRA, where that money can grow tax-free in the long term, even if you’ve surpassed the income limits that prevent you from directly contributing to a Roth. With backdoor Roth contributions, you can make a nondeductible IRA contribution of $7,500 if under 50 or $8,600 if over 50. After you have contributed to the IRA, you convert the IRA to a Roth IRA. When the funds are available in the Roth IRA, you can invest the cash in an allocation designed for growth. Equity-heavy allocation can be a great solution to get cash working towards tax-free growth. Currently, there are no income limits on non-deductible IRA contributions, which means individuals over the income limit to contribute to a Roth IRA directly can still use this backdoor Roth strategy. Reduce Taxable Income Through Charitable Giving While a noteworthy bonus may bring delight, it can also result in a higher-than-average income year and a significantly higher tax bill. You can strategically pull a few levers while you're working to minimize your tax bill – max out pre-tax retirement savings accounts, deduct property taxes up to $10,000, deduct mortgage interest on up to $1m of debt, and deduct charitable donations. Starting in 2026, provisions from the One Big Beautiful Bill Act include a 0.5% floor on charitable contribution deductibility and a cap on deductibility for those in the 37% tac bracket, creating additional complexity in tax planning. Like many of our clients, you may be charitably inclined, and making a significant charitable gift in a high-income year can be incredibly beneficial in lowering your tax bill. Some options include - direct contributions to a charity or a Donor-Advised Fund (DAF) to bundle your charitable gifts into more significant lump-sum donations. Advisor tip - To maximize the tax efficiency of your contribution, you can donate appreciated stock instead of cash. In addition, gifting appreciated stock directly to a charity or a DAF offers you an itemized deduction on your tax return and avoids the capital gains taxes on the stock. With your cash ACB payout, you can replace the stock value with cash and either reinvest in the same stock or diversify elsewhere. Optimize Your Investment Strategy by Working with a Financial Advisor Bonus payouts are definitely something to be excited about, especially if BP has had a great performance year. However, it's important to anticipate the bonuses with strategies designed to maximize opportunities for you and your family. At Willis Johnson and Associates, we can help optimize your annual performance bonus for the journey ahead through tax planning, savings prioritization, and benefits eligibility assessment. Partnering with an advisor who understands your financial needs today can be instrumental in helping you establish financial systems to support your future goals. Get started today by discussing your financial goals and BP benefits with the advisors at WJA , who can offer tailored guidance to help you reach financial independence.

Bonus time can be thrilling –having a large amount of cash on hand to fund expenses such as paying off debt, taking a vacation, or hiding it under...

READ MORE

John Siegel, CFP®, EA

SR. WEALTH MANAGER

How to Use Cash Reserves as an Emergency Fund for Retirement You’ve finally made it to retirement. You’ve achieved the goal of financial independence. Now what? In this article, we talk about making tax-efficient withdrawals in retirement. While smart withdrawals are undeniably crucial and can help optimize your portfolio in your golden years, what should you do about plain, boring cash? A common question we get from clients is: do you need to hold cash, and, if so, how much cash do you need for retirement? We believe a Cash Reserve can be an integral part of your portfolio and strategy post-retirement. Why? Having an adequate cash reserve offers emergency funds, so you have flexibility over when to sell your investments, peace of mind in times of market volatility, and comfort when spending and enjoying your hard-earned savings in retirement. How Much Cash Should You Have On-Hand in Retirement? Let’s talk about the basics: what is a Cash Reserve, and what is its strategy? As the name alludes to, a cash reserve is an account holding only cash or cash-like investments. The optimal cash-on-hand is likely between one to two years of expenses, depending on an individual’s risk tolerance and annual expenses. It is crucial to identify the right amount to have on hand because your cash reserve number needs to meet the Goldilocks standard: not too much, not too little, but just the right amount. It’s often pertinent to have enough money set aside to ride out a market downturn or accommodate your needs in a rising-inflation environment. Benefits of a Cash Reserve The Cash Reserve concept is important because it offers comfort and security in knowing where your money is coming from. Peace of Mind One of the key benefits of having a reserve is peace of mind. If you feel comfortable knowing how you’ll afford your lifestyle if there’s a dip in the market or even a recession, you will be more likely to stick with your investment strategy. Unfortunately, we see many investors without an emergency fund panic while trying to preserve their life savings. These investors get out of the market at the wrong time and make other investment mistakes that do more harm than good. Security in Your Investment Strategy On top of sticking to a long-term investment strategy, a cash reserve can also help you do what seems counter-intuitive when the market has fallen: buy. Buying at fire-sale prices and keeping funds invested can potentially augment your portfolio compared to trying to time the market. Too often, we see individuals sell out when the market is crashing and then either never get back in or get back in when the market is at all-time highs again, locking in investment losses. How Does the Stock Market Impact Your Cash Reserve? When retirees make tax-efficient withdrawals from their investment accounts during retirement, certain times in the market cycle are more beneficial than others to take these withdrawals. It’s great to take these withdrawals from your portfolio when the market is up and running, but it’s not always efficient to take them when the market is recessed. Having the right amount of cash set aside for down markets means that you can pay for expenses with the cash reserve to avoid selling invested funds at a bad time. During good times in the market, sending out systematic distributions regularly to the cash reserve helps act as paycheck replication for retirees. As the market runs, you can elect to pass distributions to a bank account for spending and covering ongoing expenses from your investments. However, during a downturn in the market, you can turn off the systematic distributions from investment accounts and live off of the Cash Reserve until the market recovers. This tax-efficient withdrawal strategy is a great way to supplement the Cash Reserve strategy over time. How to Replenish Your Cash Reserve in Retirement? A Cash Reserve can help one ride out a bad market, but we don’t wait until the market dips to think about it. When working with our clients, our goal is to continually top off the Cash Reserve to plan their cash flow and liquidity to adapt to changing market conditions. Generally, once we have decided on the right amount to keep on hand, we will set dividends and interest from a taxable account to be sent out to the Cash Reserve regularly to top off the reserve continually. Additionally, when establishing a cash reserve strategy, we want to use market run-ups to top off the Cash Reserve with distributions from an investment account if the reserves drop below an optimal amount. By leveraging market activity to fund our reserve, we can take profits and lock in gains during good times in the market rather than locking in losses by selling at bad times. Conversely, once we reach our target cash reserve threshold, any cash over and above that amount can be moved into the portfolio to be invested for future potential growth. Cash Reserves & Inflation As mentioned above, we typically believe the right amount to hold in a Cash Reserve is generally one to two years’ worth of expenses. However, that number is unique for each individual’s situation. Often, our focus with clients is ensuring enough is in their reserve for emergencies, but what about having too much set aside? After the December 2021 CPI climbed to 7%, and with banks paying minimal interest on cash, most investors were losing over 6% per year in purchasing power from their on-hand cash! With this in mind, there should be additional focus on finding the right amount to hold, not too much or too little. Common Mistakes Surrounding Cash Reserves in Retirement Let’s look at a couple of examples of how a Cash Reserve could have aided retirees, Amy and Matt, in the scenarios below. After two very successful careers, Amy and Matt reached financial independence at age 60. Together they decided to retire and use their golden years to travel all over the world, a goal they’ve been working toward since they began their careers. Together, Matt and Amy have the following assets when they retire: Matt IRA: $1,500,000 Amy IRA: $2,000,000 Joint Taxable Account: $100,000 Cash in the Bank: $20,000 For the sake of our examples later, we’ll assume a growth on the investment accounts of 8%. While working, Amy and Matt were very successful savers and had trouble spending for enjoyment, despite having steady incomes. Now that they have no salaries, they find it challenging to travel because of the mental hurdle of spending their hard-earned savings. To finance these trips, they must make withdrawals from their retirement accounts. But, because they live off their retirement accounts, they are considerably more sensitive to market fluctuations because they see market volatility as a threat to a successful retirement. Falling into the Lure of Stock Market Timing Strategies Let’s say that Matt wakes up one morning and sees that the market is down 20%. That’s a massive chunk of their retirement savings, just gone! Matt and Amy decide to go all to cash to protect the rest of their hard-earned savings. Three months later, when the market returns to where it stood initially, Amy and Matt are still afraid to re-invest since they will be purchasing at the top of the market. They will either make one of two decisions: 1) they will keep waiting and waiting for the market to dip again to buy securities at a low price, or 2) they will buy at highs in the market. Unfortunately, Matt and Amy have fallen into a common mistake by believing they can time the market. Why Trying to Time the Stock Market Doesn’t Work Matt and Amy will likely lose out on investment returns if they stay in cash instead of re-investing. However, more importantly, if they weren’t comfortable staying invested during a previous downturn, it’s unlikely Matt and Amy can convince themselves to take advantage of the next dip to get their funds re-invested. Market timing is highly debated amongst financial planners, but we believe it to be a foolish investing strategy for the long-term investor’s benefit. Bank of America looked at data from 1930 to 2020 and found that if an investor missed the S&P 500′s 10 best days each decade, the total return would stand at 28%, but if they held study over the 70 years, the return would have been 17,715%. We Talk About Market Timing and Other Common Investment Mistakes in Our Webinar, 3 Strategies to Become a Better Investor. Watch It Now >> Let’s assume Amy and Matt stay in cash for an entire year after deciding to pull their funds entirely to cash. Then, if the market still hasn’t had a pullback, let’s assume they get back in at the same prices that were available when they were fully invested. Their investments accounts, initially totaling $3,600,000, became $2,880,000 after Matt and Amy cashed out when the market dipped, a loss of $720,000! If we also assume a rate of return equaling 8%, Amy and Matt lost an additional $230,400 of growth potential from being out of the market for a year. So by being out of the market for just one year, they took a $950k hit to their retirement portfolio! Disclosures: The 8% return is derived from the historical average stock market returns for the S&P 500. The impact of investing does not represent future values of any WJA account. The deduction of advisory fees, brokerage or other commissions, and any other expenses that would have been paid is not reflected in the calculation results. Unfortunately, even if Matt and Amy decide to re-invest once the market rebounds (three months later), they will still lock in the $720,000 in losses they took earlier. Both of these decisions have the potential to de-rail their retirement, precisely what they were trying to avoid! Spending Beyond Your Retirement Budget Let’s switch up the example to another scenario we often see with people we meet with. What if, instead of being conservative spenders, Amy and Matt have a habit of spending beyond their means and don’t have a good idea of their retirement budget? Between obligations and spending, Matt and Amy need to continue making withdrawals from their accounts even during a downturn in the market. What if they need $300,000 this year ($25,000 per month) for expenses and the market averages a 25% loss across those 12 months? In this scenario, Matt and Amy face losses of $75,000. While this may not seem like a lot, these losses will add up over time if they continue to make withdrawals during market dips in the future, which can impact their retirement savings and goals. Cash Reserves can Offer Investment Opportunities How could these situations have been avoided, and what could Matt and Amy do differently? If instead, Amy and Matt had additional cash set aside to cover 1-2 years of expenses, rather than only $20,000, they may have felt more comfortable with the dip in the market. While pullbacks are always slightly uncomfortable, a Cash Reserve makes the uncertainty more manageable. In addition, having an emergency fund set aside allows Amy and Matt the security to sleep at night during the market volatility because they know they have at least two years’ worth of expenses and trip costs set aside to carry them through this downturn. With this peace of mind, they can also see the opportunity this downturn presents to buy on the dips at great prices. Then, as they ride the market back up, Matt and Amy will be in an even better place financially than they were before the dip. While these fictional scenarios are great, let’s confront a real-life example we all can relate to — March of 2020. Using Your Emergency Fund During Market Downturns Cash reserves were the financial heroes for our clients during the COVID recession. When the market dropped in March of 2020, no one knew when it would rebound. The onset of a global pandemic was scary, and the global financial impact was unknown. The cash reserves strategy helped our clients sleep at night during this period of uncertainty, knowing they were prepared for this exact moment. With each client, we review the Cash Reserve strategy leading up to their retirement. We decide the proper amount of cash to set aside and strategically send systematic distributions into the reserve with dividends and interest when the market is thriving. In addition, we have education sessions on why these reserves are significant and how they can help us make good decisions during market volatility. In addition to staying invested, we took the market drop as an opportunity to help clients add to their investments by buying asset classes that fell substantially during the drop. Leveraging market momentum through target band rebalancing worked exceptionally well for our clients as they rode the market back up and took advantage of recently-rebounded market areas. Though no one knew how quickly the market would recover, and it recovered more rapidly than expected, the cash reserve strategy allowed us to leverage opportunities in the market by staying invested. We’ve had excellent market performance following the initial COVID market drop in February 2020, but our job now is to prepare clients for whenever the next market dip occurs, to make sure our reserves are topped off, and to make sure the emergency fund can carry them through the next period of volatility. A Cash Reserve can be an essential part of your retirement plan. Ask yourself this: Will you be ready for the next market drop, and how will you handle it? Could having a cash safety net help you be a better long-term investor? Could the cash reserves strategy help you budget and rebalance your portfolio regularly? Could having cash set aside for expenses encourage you to buy when things are scary in the market? Efficiently structuring your financials during retirement can allow you to enjoy what you’ve worked so hard for while feeling secure about the market and making withdrawals to enjoy this new chapter in your life. At Willis Johnson and Associates, we look at the pieces of your financial picture together to ensure nothing gets overlooked. We believe that a cash reserve can be an essential piece of everyone’s financial picture. Together, we can review the optimal amount of cash to hold based on annual expenses in conjunction with your risk tolerance. We have found that those with Cash Reserves have better investment returns over the long run because there is no concern about where funds will come from to cover expenses in a down market. Additionally, the comfort of knowing that cash is available helps decrease reactivity to the market when we see a pullback, allowing funds to stay invested and continue to grow and compound over time. This strategy can make a substantial difference in your portfolio over time when done correctly. Working with a financial advisor is beneficial to determine if this or other tax-efficient savings strategies can help you reach your long-term goals. Start the conversation with an advisor today.

You’ve finally made it to retirement. You’ve achieved the goal of financial independence. Now what? In this article, we talk about making...

READ MORE

Sarah Sikorski, CPA, CFP®

DIRECTOR, WEALTH MANAGEMENT